2026/27 Federal Budget Recap – Key Changes in Simple Terms

Property Investors – Negative Gearing Changes

From 1 July 2027, negative gearing rules are proposed to change for future residential investment properties.

What’s changing?

- Negative gearing will only apply to newly built residential properties purchased after 12 May 2026.

- For existing residential properties purchased after this date, rental losses will no longer reduce your wage or other income.

- Instead, those losses will be carried forward and used against future rental profits or capital gains.

Important:

If you already own an investment property before 12 May 2026, these changes will not affect you.

What this means for you:

Future property investments may need more careful planning and cash flow consideration. These changes do not apply to self-managed super funds (SMSFs), commercial properties, or shares.

Capital Gains Tax (CGT) Changes

From 1 July 2027, the current 50% CGT discount is proposed to change for newly purchased assets.

What’s changing?

- The 50% CGT discount will no longer apply to assets purchased from 1 July 2027 onwards.

- Instead, asset costs will be adjusted for inflation (indexation).

- A minimum 30% tax rate may apply to capital gains after indexation.

Important:

Assets purchased before 1 July 2027 will keep the current 50% discount on gains accrued up until that date.

What this means for you:

Selling investments such as property or shares in the future may result in higher tax than under the current rules. Companies and SMSFs are not affected by these proposed changes.

Discretionary Trust Changes

From 1 July 2028, discretionary trusts (commonly known as family trusts) may face new tax rules.

What’s changing?

- Trust distributions may be taxed at a flat 30% rate.

- Beneficiaries will receive a tax credit for tax already paid by the trust.

- Some trusts are excluded, including super funds, deceased estates, fixed trusts, primary production income, and existing testamentary trusts.

What this means for you:

Trusts will still provide asset protection and succession planning benefits, but they may become less effective for reducing overall family tax. There is still time before these rules commence, and restructure relief is expected to be available if changes to your business structure are needed.

Business Owners

What’s changing?

- The $20,000 instant asset write-off is now proposed to become permanent.

- Businesses may have the option to pay PAYG instalments monthly instead of quarterly.

What this means for you:

This provides more certainty when purchasing business assets and may assist with managing business cash flow.

Salary & Wage Earners

What’s changing?

- A new $250 tax offset is proposed from the 2027–28 financial year.

- Employees may be able to claim up to $1,000 of work-related deductions without keeping receipts.

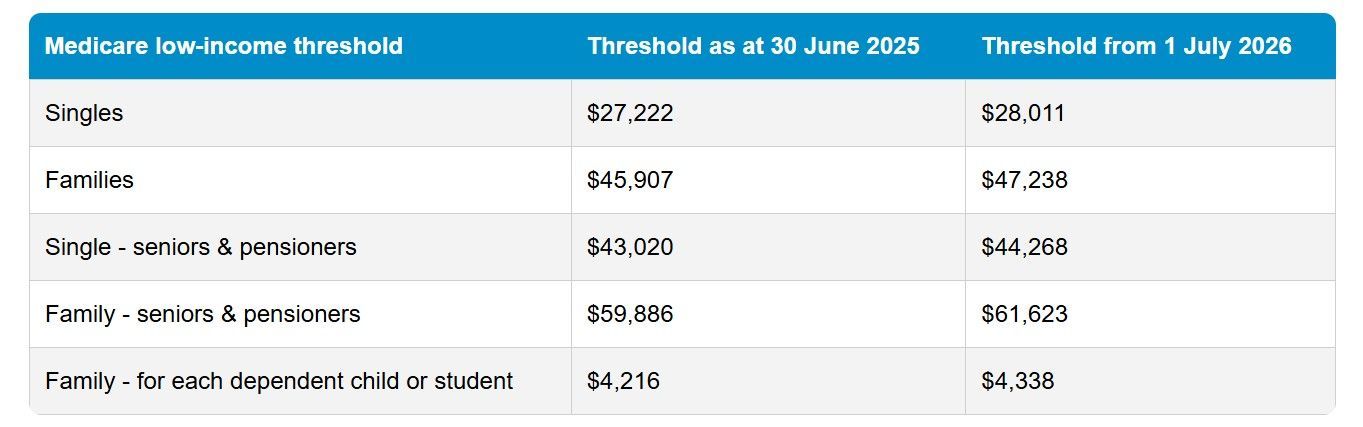

- Medicare levy low-income thresholds will increase.

What this means for you:

Most employees may receive small tax savings and a simpler tax return process.

Medicare Levy Threshold Increases

Final Comments

While the 2026/27 Federal Budget may not contain as many changes as the AFL rulebook lately, there are still some significant proposed tax reforms that could affect individuals, investors, and small business owners.

Importantly, these measures are still proposals only and will need to pass Parliament before becoming law. Further detail and clarification are also expected over time.

We encourage clients to contact us to discuss how these proposed changes may affect their personal circumstances. We will continue to keep clients updated as further announcements are made.